The Timken Company (NYSE: TKR) has spent the better part of 2026 rewriting its own story. The stock is up roughly 87% over the past year, and for the first time in a while, the fundamentals are actually keeping pace with the price. This TKR stock analysis breaks down what is driving the move, where the valuation stands today, and whether the Timken stock 2026 outlook still makes sense for investors entering at current levels.

The 80/20 Strategy Is the Whole Story

If you want to understand TKR right now, you have to understand the 80/20 operating model. Timken is actively pruning its lower margin businesses and doubling down on the ones that generate the most value. The clearest signal of this was the announced sale of the belts business to Gates Industrial, which is expected to close in Q3 2026. At the same time, the company acquired Bijur Delimon International in March 2026 to build out its lubrication platform, which now sits at over $400 million with a clear runway toward $500 million.

This is not a company sitting still. The portfolio transformation is designed to push adjusted EBITDA margins from current levels toward a 21 to 23 percent range by 2028, with revenue targets of $5 to $5.2 billion and free cash flow of $1.3 billion over that same period.

That is the Timken stock outlook that the market is currently pricing in, and Q1 2026 gave investors real evidence it is achievable.

Q1 2026 Earnings: The Beat That Justified the Rally

Timken reported Q1 2026 results on May 6, 2026. Revenue came in at $1.23 billion, up 8 percent year over year. Adjusted EPS landed at $1.67 against analyst expectations of $1.51, which was an 11 percent beat. Net income margin expanded to 8.0 percent from 6.9 percent in Q1 2025. Adjusted EBITDA margin improved to 18.8 percent.

The company followed the earnings beat by raising its full year 2026 guidance. Diluted EPS is now expected in the range of $4.70 to $5.20, up from the initial guidance of $4.50 to $5.00. Adjusted EPS guidance sits at $5.75 to $6.25.

Earnings growth of 26.1 percent year over year tells you the core business is genuinely accelerating. For a TKR stock analysis at this stage, that kind of bottom line momentum matters more than surface level revenue numbers.

Valuation: Fair Value or Fully Priced?

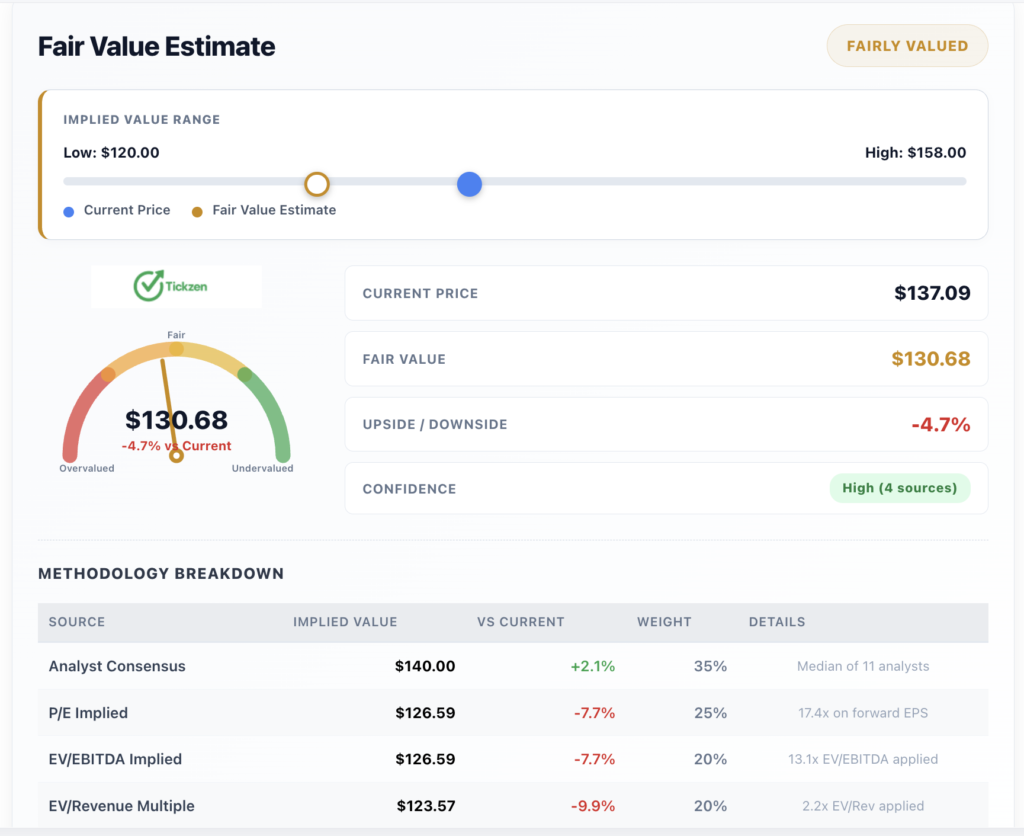

At $137.09 (as of June 10, 2026), the question every investor has to answer is whether TKR stock is a good buy at current prices or whether the rally has already baked in the good news.

The forward P/E sits at 18.89x, which is reasonable for a high quality industrial with accelerating earnings. The trailing P/E of 31.16x looks stretched but that is largely because earnings are in a phase of rapid expansion. The PEG ratio of 1.86x sits in a moderate zone, not cheap but not wildly expensive for a company executing this well.

Tickzen.app’s blended fair value estimate for TKR comes in at $130.68, which puts the current price about 4.7 percent above that figure. The 11 analyst consensus puts the mean price target at $136.55 with individual targets ranging from $120 to $158. Evercore ISI has the most bullish target at $158, and they carry an Outperform rating.

The honest assessment: TKR stock is not cheap. It is fairly valued to modestly stretched depending on which methodology you weight. The investment case rests on whether the 2028 margin targets are credible, not on a near term discount to intrinsic value.

More From Tickzen:

- American Airlines Stock (AAL) Technical Analysis 2026

- Is IREN Stock Overvalued at $61? What the Numbers Say Before You Buy

- EchoStar SATS Stock Analysis 2026: Is the 7x Rally Running Out of Steam?

- FuelCell Energy, Inc. (FCEL) Technical Analysis 2026: 12-Month Forecast & Key Risks

- Is Broadcom Stock Worth Buying at $446? AVGO Valuation and Fundamentals

Financial Health Gives the Bull Case Room to Run

Before calling TKR stock a good buy, the balance sheet deserves attention. The debt load of $2.20 billion is real and worth watching, particularly with the Debt to Equity ratio sitting at 0.65x. That said, the company generated $535 million in operating cash flow over the trailing twelve months, and levered free cash flow sits at $338 million. The current ratio of 2.88x shows strong short term liquidity.

Return on equity of 10.28 percent and return on invested capital of 6.04 percent are moderate, not exceptional. Gross margin of 30.60 percent and operating margin of 14.03 percent show a business that controls costs and converts revenue effectively. The compression between gross margin and net margin (30.60 percent versus 6.60 percent) is largely a function of interest expense tied to the debt load, which management has indicated will ease as portfolio divestitures generate cash.

Institutional ownership at 95.47 percent tells you that sophisticated capital is not running from the stock. JPMorgan upgraded TKR to Neutral with a $130 target in May 2026. Goldman Sachs raised its target to $128. Oppenheimer, who has been consistently bullish, has a $158 target alongside an Outperform rating.

End Markets Are Opening Up

Timken’s core Engineered Bearings segment serves wind energy, agriculture, aerospace, automotive, and rail. The Industrial Motion segment adds solar energy, automation, packaging, medical, and marine exposure.

Industrial automation and the growing demand for precision components in electric vehicles and humanoid robotics represent legitimate long term tailwinds that are just beginning to influence Timken’s order book. Management specifically called out humanoid robotics exposure in recent commentary. These are not speculative end markets for a company that makes the components that keep those systems running.

Revenue growth of 8 percent year over year in Q1 2026, driven by improving customer demand across several end markets, signals that the cyclical recovery in industrials is working in Timken’s favor at the same time the structural portfolio improvements are landing.

What to Watch Before the Next Earnings

The next TKR earnings date is July 29, 2026. That report will be the first real test of whether the Q2 environment sustained the Q1 momentum. Key metrics to watch include adjusted EBITDA margin progression toward the 2028 targets, any update on the belts business sale timing, and order trends in aerospace and automation end markets.

The ex dividend date of May 19, 2026 has already passed. The annual dividend sits at $1.44 per share, yielding 1.05 percent at current prices. The payout ratio of 31.82 percent is healthy and leaves substantial room for future increases. Income investors should not buy TKR for the yield alone, but the consistent dividend is a signal of management confidence in cash generation.

Want to see whether this stock is still a buy at current levels? Run the full analysis to check fair value estimates, insider activity, technical signals, options positioning, support and resistance zones, and what analysts are expecting next in seconds.

The Bottom Line for Investors

Timken is in the middle of a real transformation, not a rebrand. The 80/20 strategy is shedding low margin drag, the Bijur Delimon acquisition deepens a platform with clear scale economics, and Q1 2026 delivered the kind of earnings beat that validates the thesis rather than just the hype.

The Timken stock 2026 outlook is constructive for patient investors who are comfortable with moderate valuation and an industrial growth story tied to automation and precision motion technology. At $137.09, TKR is not a discount purchase. But for investors who want exposure to a well managed industrial with a credible three year margin expansion roadmap, the TKR stock forecast through 2028 remains compelling.

This article is for informational purposes only and does not constitute investment advice. Always conduct independent research before making investment decisions.

Comments

Join the discussion and share your view on this insight.

No comments yet. Be the first to contribute.